Getting a vaccine is a “top priority” and “we’re going to get it taken care of.” However, the virus will probably “get worse before it gets better.”

—Donald Trump, July 21, 2020

“There’s no point in pumping air into a leaky tire…in a pandemic economy, stimulus alone cannot trigger a full recovery.”

—Dr. David Kelly, JPMorgan, July 20, 2020

Key takeaways

- As of July 24, 2020, there were more than 4.05 million cases and over 144,000 deaths in the United States. Worldwide, there have been more than 15.56 million cases and over 634,000 deaths. (Johns Hopkins University)

- The prospects of successfully developing a coronavirus vaccine as soon as this year were buoyed last week when the world’s leading candidates reported positive early trial data. The U.S. government will pay nearly $2 billion for Pfizer and BioNTech to produce and deliver 100 million doses of their Covid-19 vaccine, with the option to buy another 500 million doses. (Wall Street Journal, LPL Financial)

- According to Gavekal, U.S. infections should peak by mid-August. Their model predicts an upper bound of 140,000 infections per day with a mean of 75,000 infections per day. (Gavekal)

- According to the Labor Department, 20% of the U.S. labor force is collecting unemployment benefits.

- Gregory Daco of Oxford Economics believes that “the risk of a relapse in demand is rising.” His research has found that confirmed infections are rising in 39 states which together account for 90% of the U.S. economy. (Wall Street Journal)

- Goldman Sachs believes that face mask mandates can help avoid further GDP loss.States with face mask mandates have lowered their infection growth rates by 25%. According to Goldman, opting for masks versus national lockdown equates to avoiding a -5% GDP contraction. (Goldman Sachs Asset Management)

- Consumer sentiment declined to 73.2 in July, down from the prior reading of 78.1. The survey estimated sentiment to be 79.0, but the actual was off by -5.8. (University of Michigan)

Will stocks hurdle a limbo-low earnings bar?

| U.S. Stock Market Data |

| 7/24/2020 Close |

Week |

YTD |

1-year |

| S&P 500 |

3,215.66 |

-0.28% |

-0.47% |

-0.76% |

| NASDAQ |

10,363.18 |

-1.33% |

+15.50% |

+24.40% |

| DJIA |

26,469.68 |

-0.76% |

-7.26% |

-2.66% |

Source: MarketWatch

Trending: How sustainable is the run-up from Amazon, Apple and Microsoft?

Amazon has surged +61% this year, with investors piling in to escape the carnage elsewhere in the market. Apple and Microsoft are up +27% and +29%, respectively.

The dizzying rally in these stocks has propelled the Nasdaq Composite Index up +15.5% this year, setting 28 record closes along the way. The S&P 500, meanwhile, has recouped almost all of its losses for the year, and is now down just -0.47%.

Investors say the shift makes sense because changes in consumer behavior during the pandemic have been a boon to the business models of many of the big tech companies.

Still, analysts caution investors against becoming too complacent by betting that big tech stocks have nowhere to go but up when their valuations are already elevated. The pace of the rally, after the brutal selloff of February and March, and the increasing influence on the market of a handful of stocks, have given other investors pause. (Wall Street Journal)

1. Market update

- This week, the S&P 500 was -0.28%, the Nasdaq was -1.33%, and the Dow Jones was -0.76%.

- Year-to-date, the S&P 500 is just about flat. As of Friday, June 24, 2020, the Index is -0.47%. The Nasdaq is +15.50% and the Dow Jones is -7.26% since the beginning of the year.

- The forward P/E ratio is 22.44x as of July 23, 2020. It has not been this high since the tech bubble in 2000 and is well above the 25-year average of 16.4x. (JPMorgan Asset Management)

2. Covid-19 summary

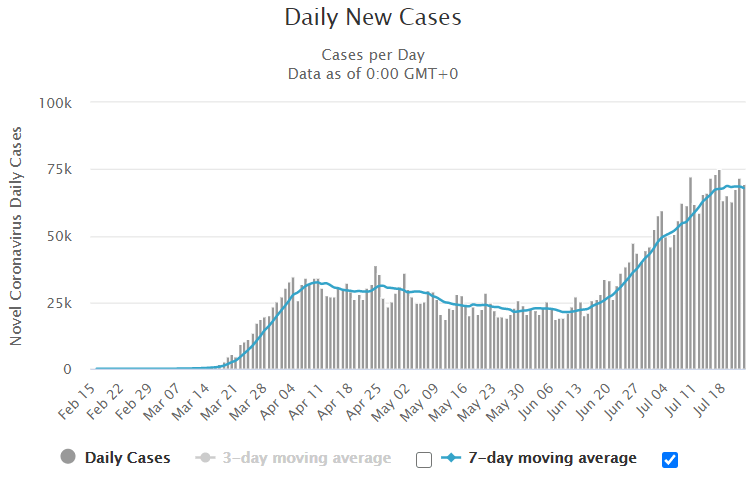

Figure 1: Daily New Covid-19 Cases in the U.S. as of July 24

Source: worldometers&v=gsp2uwp2prlbhfzfn32byfmj

- As of July 24, 2020, there were more than 4.05 million cases and over 144,000 deaths in the United States. Worldwide, there have been more than 15.56 million cases and over 634,000 deaths. (Johns Hopkins University)

- New cases in the United States totaled just under 69,000 on Thursday, July 23, 2020, down 11.1% from a week ago, though on 6.1% fewer tests. The stability in the seven-day average of new daily cases—up 1.4% week-over-week—suggests the curve may have been flattened. (Johns Hopkins University, LPL Financial)

- The prospects of successfully developing a coronavirus vaccine as soon as this year were buoyed last week when the world’s leading candidates reported positive early trial data. The U.S. government will pay nearly $2 billion for Pfizer and BioNTech to produce and deliver 100 million doses of their Covid-19 vaccine, with the option to buy another 500 million doses. (Wall Street Journal, LPL Financial)

- According to Gavekal, U.S. infections should peak by mid-August. Their model predicts an upper bound of 140,000 infections per day with a mean of 75,000 infections per day. (Gavekal)

- Gavekal also estimates that deaths will peak between late August and mid-September, as their model has an upper forecast of 1,900 deaths per day with a mean estimate of 1,000 per day. (Gavekal)

- Goldman Sachs believes that face mask mandates can help avoid further GDP loss. States with face mask mandates have lowered their infection growth rates by 25%. According to Goldman, opting for masks versus national lockdown equates to avoiding a -5% GDP contraction. (Goldman Sachs Asset Management)

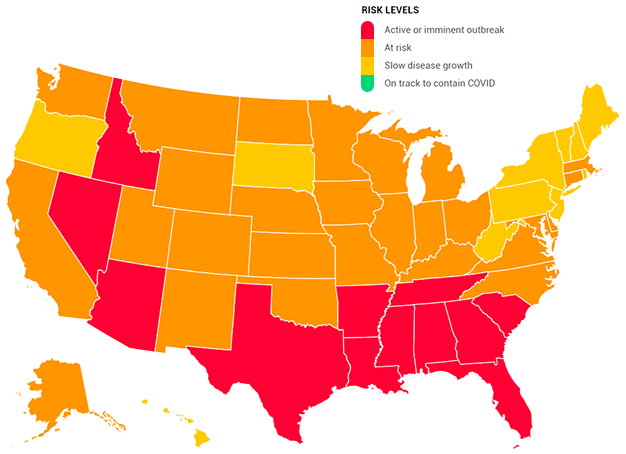

- Zero (0) states are on track to contain Covid-19. Eleven (11) states are experiencing an active or imminent outbreak, and twenty-seven (27) states are at risk of an outbreak. (Covid Act Now)

Figure 2: State of the States

Source: Covid Act Now

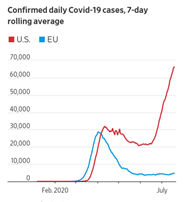

3. Europe’s ‘Hamilton moment’

Coronavirus cases were expected to surge as reopenings across Europe began this Spring.

As you can see, they have not. Much of the success in containing the virus can be attributed to significant changes in social behavior.

According to the Wall Street Journal, Europeans almost universally wear masks, keep their distance when possible, and focus heavily on personal hygiene.

European Union leaders agreed on a €1.8 trillion ($2.06 trillion) spending package aimed at containing an unprecedented economic downturn by resorting to new measures that could ultimately deepen the bloc’s economic integration. The package, built around the bloc’s first-ever issuance of hundreds of billions of euros of common debt, came together after talks among the bloc’s 27 leaders.

European leaders have also agreed to a €750 billion ($858 billion) stimulus plan that will provide additional funding beyond what national governments have allocated to help the continent’s economy recover from Covid-19. The fund is the biggest joint borrowing ever agreed on by the EU. (Wall Street Journal, Barron’s)

4. What is going on in the economy right now?

- Consumer sentiment declined to 73.2 in July, down from the prior reading of 78.1. The survey estimated sentiment to be 79.0, but the actual was off by -5.8. (University of Michigan)

- Total mortgage applications activity climbed +4.1% last week, and the breakdown between new purchases (+2.0%) and refinance activity (+5.0%) was not as lopsided as last week when home-buying activity fell -6%. New home purchase activity is up +19% year-over-year, while refinance activity has soared +122% year-over-year. (Cetera Investment Management)

- Existing home sales jumped +20.7% month-over-month, the first rebound in four months. Existing home sales are down -3.4% year-over-year, however. (Cetera Investment Management)

- U.S. business activity increased to a six-month high in July. U.S. PMI Manufacturing rose to 51.3 in July, up from 49.8, marking a 6-month high. PMI Services rose to 49.6, up from 47.9, also a 6-month high but stayed in contraction. PMI Composite rose to 50.0, up from 47.9. (IHS Markit)

- Gregory Daco of Oxford Economics believes that “the risk of a relapse in demand is rising.” His research has found that confirmed infections are rising in 39 states which together account for 90% of the U.S. economy. (Wall Street Journal)

- Gold prices advanced to $1,880 per ounce last week, moving closer to its $1,921 all-time high set back in 2011. Gold is up about +25% year-to-date.

5. Unemployment

- Initial claims for jobless benefits unexpectedly rose by 109,000 last week to 1.416 million. This was the first increase in 16 weeks.

- Continuing claims decreased week-over-week to 16.197 million from 17.304 million in the prior week.

- According to the Labor Department, 20% of the U.S. labor force is collecting unemployment benefits. The Household Pulse Survey suggests that the labor market rebound peaked in mid-June and has been reversing since. (Census Bureau)

- The looming expiration of the federal “top-up” of $600 per week in unemployment insurance (UI) benefits represents a major income cliff worth $1.2 trillion, equating to $800 per family. Unfortunately, income cliffs cause major risks to the economy. Oxford Economics estimates a -6% decrease in personal income when the UI “top-up” benefits expire. (Oxford Economics)

6. JPMorgan Chase: ‘There clearly are still opportunities for long-term investors’

- Dr. David Kelly, chief global strategist at JPMorgan, believes that since the S&P 500 is nearly unchanged for the year, it suggests “a risk of a correction.” However, there are still opportunities in the long-term even though the current “V-shaped” recovery has been interrupted.

- Dr. Kelly said that “it still looks like 2021 will be a year of recovery for the economy and corporate earnings.” This suggests the need to hedge against equity volatility in the short run while maintaining equity exposure to take advantage of an economic surge once Covid-19 has been tamed.

- According to Dr. Kelly, there are many countries around the world, particularly in East Asia, and more recently in Europe, that have done a better job in corralling the virus. This should allow their economies to continue with a phased reopening, with less damage done to their economies and public finances. “For those who are underweight international equities, this may be a good time to consider increasing exposure to companies than can benefit from economic revival in these countries,” says Dr. Kelly. (Dr. David Kelly, JPMorgan Asset Management, Financial Advisor Magazine)

7. Bullish thinking

- Goldman Sachs predicts that the S&P 500 will gain +6% annually during the next 10 years with a one standard deviation range of 2%–11%. Goldman notes that their equity return forecast combined with the current record low 0.63% 10-year Treasury yield suggests stocks have a greater than 90% likelihood of outperforming bonds through 2030. (Goldman Sachs Asset Management)

- BlackRock said that Europe offers the “most attractive regional exposure” as the global restart gathers pace. A growth pickup would typically benefit emerging markets, it said, but in this instance, Europe’s robust health infrastructure and policy response left it better placed. (MarketWatch)

8. Bearish thinking

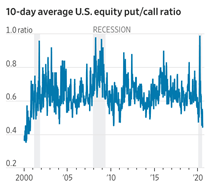

- The 10-day moving average of put/call ratios shows the least use of puts relative to calls since September 2000, when the post-tech bubble selloff began in earnest. As you can see, it has rarely shown as much optimism as it is showing now. (Wall Street Journal, Refinitiv)

- Trading volumes on the technology-heavy Nasdaq compared with the NYSE tell a similar story. They are rising in a way reminiscent of the technology bubble.

- BlackRock remained neutral on U.S. equities, citing “the risk of fading fiscal stimulus and election uncertainty,” and overweight on European stocks after upgrading the region in its midyear outlook. (MarketWatch)

- Goldman Sachs expects trends of deglobalization to pressure earnings in the upcoming decade. (Goldman Sachs Asset Management)

- Elevated cyclically adjusted price-to-earnings multiples (CAPE ratios) have historically indicated lower future returns. At today’s multiple of 29x, which has occurred less than 1% of the time, total returns have averaged 6% the following decade. (Goldman Sachs Asset Management)

- On average, July 31 marks the start of the worst 60-day stretch for U.S. equities. The 60-day rolling forward return on July 31 is -0.7% since 1990. (Bloomberg, Morgan Stanley Research)