Aided by massive stimulus and liquidity injections from the Fed, the S&P 500 Index has turned positive for the year. Cautiously upbeat headlines regarding a vaccine have also supported sentiment. Yet, tensions between the U.S. and China are rising, and the coronavirus-inspired fog of uncertainty has yet to lift.

The strength of the economic rebound in May and June has been more than almost anyone could have anticipated. Record gains in employment and retail sales suggest early investor optimism wasn’t misplaced, at least so far.

Given projections that earnings will begin to recover next year, investors appear to be looking beyond 2020. Further, longer-term Treasury yields well below 1% are supportive of richer multiples. Still, let’s not discount the possibility we could see renewed volatility.

Two months doesn’t make an economic recovery. The spike in COVID-19 cases and the path of the disease, doubts about the size and make up of any new fiscal stimulus, and the plateauing of high frequency data suggest a rockier road ahead, at least in the near term.

1. The good news

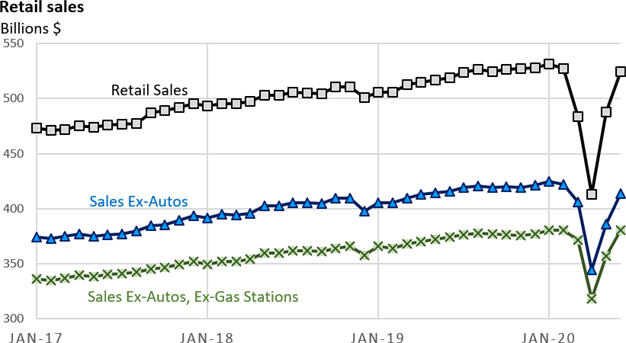

- Retail sales easily exceeded expectations in May and June following a record drop in April.

- May and June were the best performing months on record, with data beginning in 1992.

- If there ever was a V-shaped recovery, Figure 1 highlights such a bounce.

- Credit business reopenings, stimulus money (including generous jobless benefits), and pent-up demand.

- Spending on autos hit a record in June.

Figure 1: V-Shaped Bounce to Near Pre-COVID-19 Levels

Source: U.S. Census June 2020

- However, risks abound.

- Can spending continue at pre-pandemic levels with an unemployment rate above 10%? A continuation of generous jobless benefits and new stimulus would lend support, but medium and longer term, a sustained recovery in jobs is needed.

- Generous jobless benefits are a double-edged sword. The cash supports spending but can discourage furloughed workers from returning to work

- Backtracking or delays in reopenings in some states, still-high unemployment, and renewed worries about the spike in COVID-19 cases are headwinds to further gains.

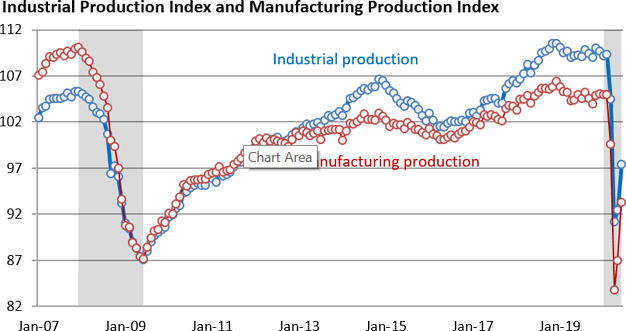

The industrial sector

- The manufacturing sector has been slower to get cranked up following a record decline in April; nonetheless, the bounce in May and June has been impressive.

- June’s rise in industrial production (5.4%) was the biggest increase since 1959 (data back to 1919).

- June’s rise in manufacturing production (7.2%) was the biggest since 1946.

- Industrial production has recovered one-third of its March/April decline in just two months.

- Manufacturing production has recovered almost one-half of its March/April decline.

- Early July surveys by regional Fed banks suggest further gains in production are on tap, but manufacturing is being hindered by pain in the oil industry.

Figure 2: An Industrial Bounce

Source: Federal Reserve, NBER Shaded areas mark recessions June 2020.

Manufacturing production accounts for 75% of industrial production.

Manufacturing production excludes electricity and mining production.

- Consumer spending and manufacturing are highlighted as they are key pillars of support for the economy.

- Both are exhibiting a V-shaped bounce thanks to government stimulus and the easing of lockdowns.

A broad-based indicator confirms the bounce

- The Chicago Fed National Activity Index, which is comprised of 85 monthly economic reports, recorded a record +4.11 in June versus +3.50 in May (a record at that time), which follows a record collapse of -18.09 in April.

Near-term caution

- High-frequency economic reports are suggesting a plateau over the near term.

- The rebound in restaurant bookings has stalled (per OpenTable) and remain well below pre-pandemic levels. Social distancing requirements are likely to hamper sales for the foreseeable future.

- Requests for directions have stalled (Apple Maps).

- Improvement in travel through TSA checkpoints has leveled off (TSA) and remains well below pre-pandemic levels.

- Improvement in hotel occupancy rates has slowed (Hotel News/STR) and remains well below pre-pandemic levels.

- The recovery in foot traffic to businesses has stalled and remains below pre-pandemic levels (SafeGraph).

- Mid-July consumer sentiment unexpectedly declined (U Michigan survey).

- Silver lining—for the most part, we’re seeing a plateau in the daily/weekly reports and not a decline, which would resemble a W-shaped path.

- While the situation remains fluid, might a ‘square-root’ recovery be in the making, i.e., a sharp bounce followed by a plateau?

- The path of the virus will prominently influence the recovery.

2. PPP lifeline

- There has been no shortage of headlines highlighting how celebrities, movie stars, and rock bands have received loans under the Paycheck Protection Program.

- Recipients include Kanye West, Reese Witherspoon, Guns N’ Roses and the Eagles.

- The program was designed so that small businesses could make rent payments and keep employees on the payroll. While we can debate whether celebs should be receiving taxpayer funds, let’s look beyond eye-catching headlines.

- Through July 17, the Small Business Administration said it has approved

- 4.95 million loans

- Loans totaling $518.3 billion dollars

- Average loan size of $104,699

- Furthermore,

An imperfect program and overlooked successes

- Businesses that received the loans employ over 51 million people or 84% of all small business employees.

- PPP enabled many nonprofit organizations to access loans to support their employees. Traditionally, nonprofits are not eligible to receive SBA-guaranteed loans.

- Crafted at the height of the economic crisis, the program has had its share of blemishes, and some folks received loans that otherwise shouldn’t have.

- Additional headlines that shine a negative light on the program may continue to pop up.

- Yet, let’s not let overlook the tremendous benefits to small businesses and the economy amid a crisis that forced closures of “nonessential” firms through no fault of their own.

- Per the Fed’s July , the “PPP and loan deferrals reportedly provided many firms with sufficient liquidity for the near term. Outlooks remained highly uncertain, as contacts grappled with how long the COVID-19 pandemic would continue and the magnitude of its economic implications.”

3. Jamie Dimon and limited visibility

- The view is obscured by a thick fog.

- Many analysts could provide a bullish case or a bearish case. But conviction would be low.

- In late May said, “You could see a fairly rapid recovery,” amid support from stimulus.

- Six weeks later, he’s changed his tune.

- “If you look at the base case, an adverse case, an extremely adverse case, they’re all possible and we’re just guessing at the probabilities of those things; that’s all we’re doing,” he said.

- “You’re going to have a much murkier economic environment going forward than you had in May and June, and you have to be prepared for that.”

- “We simply don’t know,” Dimon added, “and, by the way, we’re wasting time guessing.”

4. Answering questions without answers

With slight modifications, these appeared in June’s Advisor TalkingPoints and they are still relevant.

- How quickly can COVID-19 be brought under control?

- Are the current spikes temporary? How quickly might they play out?

- Will we experience a second wave this coming fall and winter?

- How long will it take for confidence to return and normal spending to resume?

- How might businesses that require person-to-person interactions fare over the medium and longer term?

- When will an effective treatment and an effective and readily available vaccine be developed? Will either be developed?

Forecasting is difficult even in “normal” times. The questions above don’t have readily available answers; therefore, modeling outcomes are filled with guess work.

5. A peek ahead

I. Q2 GDP will be the worst ever

- There is a projected 31.9% annualized decline in Q2 per the WSJ Economic forecasting survey.

- Investors have already braced for a bad Q2. Without trying to diminish the uncertainty and pain felt by many, GDP is a rearview-mirror report: April–June. We’re about to enter August.

- The outlook remains unusually uncertain, but forecasters are looking for a record 15.2% rebound in Q3 and a 6.8% rise in Q4.

- While the projected rebound is encouraging, updates to the forecast may be more important as visibility is limited and projections at this point may simply be educated guesses.

- Upgrades would suggest a more optimistic outlook; downgrades would suggest a more sober view.

II. Earnings in view

- Q2 S&P profits are projected to fall 41.2% versus a year ago (Refinitiv as of 7/22/2020 with 15% having reported).

- It’s still early, but firms are topping a low hurdle.

- 77% of companies that have reported have beaten the consensus estimate and have beaten by a wide margin.

- With limited guidance, analysts are too conservative, at least in the early stages.

- Revenues are projected to fall 10.7%

Looking ahead

- Q3 2020 profit forecast: -23.9% versus -24.9% one month ago

- Q4 2020 profit forecast: -12.8% versus -13.1% one month ago

- Q1 2021 profit forecast: +11.7% versus +11.7% one month ago

- Q2 2021 profit forecast: +63.3% versus 64.8% one month ago

- Forecast in today’s environment are subject to significant changes, but an expected profit recovery next year has been a tailwind for stocks.