Editor’s note: This year we are presenting some of the most popular articles of the year that didn’t quite make it into our Top 10, but still got a lot of attention because of their unique topics. We think you’ll enjoy taking another look at these interesting runners-up!

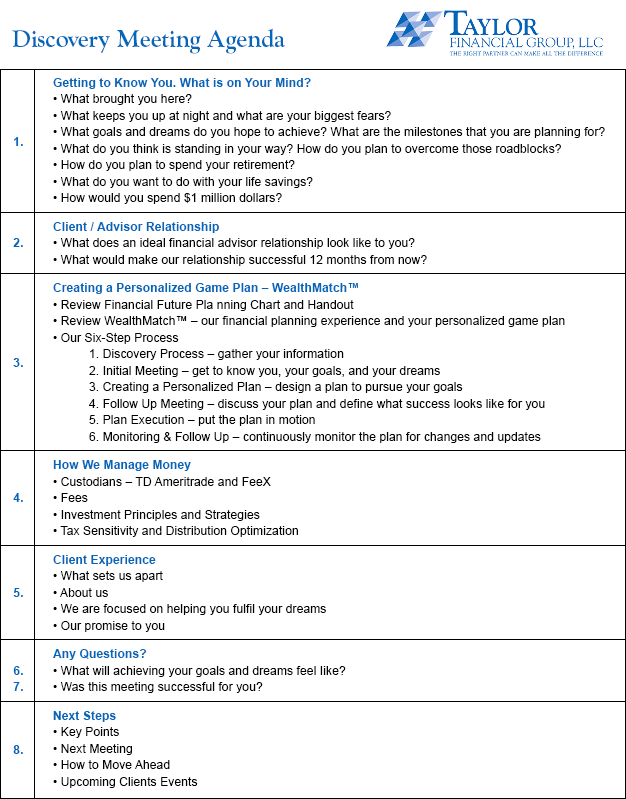

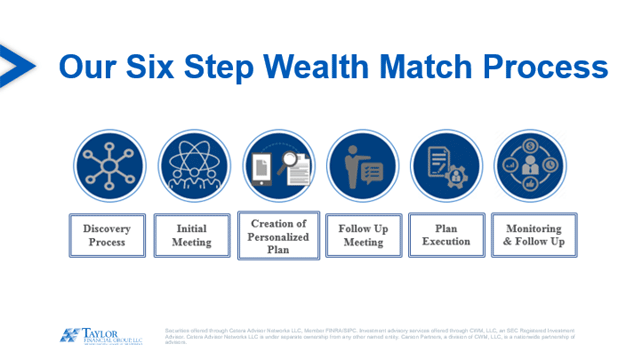

Before a client commits to any financial advisor, they want to make sure they are hiring the best person for their situation. You and the prospective client need to get to know one another before working together. Creating a discovery meeting agenda is the first step in ensuring all important areas of concern are covered. Below you will see the agenda we use at Taylor Financial Group (TFG) for our discovery meetings.

Figure 1: Have an Agenda for the Discovery Meeting

Source: Taylor Financial Group

The 12 questions

Whether a prospect is creating a vision for retirement, looking to finalize their estate plan, or planning to retire soon, every advisor should be prepared to address the following 12 questions during the discovery interview process. Following are our recommendations for generating your own answers, along with slides from the TGF presentation covering these topics.

1. What are your qualifications?

For some prospects, specific credentials can be critical. There are endless numbers of certifications and qualifications that an adviser can acquire. Whether you as the advisor possess these credentials or a member of your staff does, having earned some letters to put behind your name is a plus for most prospective clients.

Practice tip: We have noticed our prospects are most interested in CFP and CPA, particularly given the tax climate. How are you differentiating yourself with prospects?

Figure 2: How Do You Differentiate Yourself?

Source: Taylor Financial Group

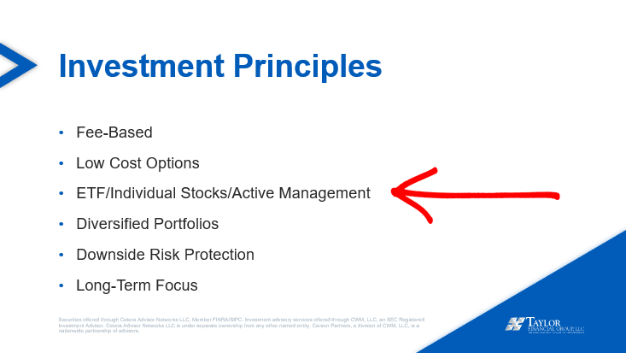

2. What is your investment philosophy? Are there any limitations on the investments you will recommend?

Investments play an essential role in a prospect’s overall financial health, and they want to work with an advisor who uses methods they are comfortable with. Make sure as the advisor that you have a clear, evidence-based strategy that you can communicate so that prospects easily understand it.

Practice tip: The advisor should clearly articulate their investment philosophy, strategy, and principles using an evidence-based methodology. If this isn’t the case, prospects may suspect that investment management isn’t receiving the attention it deserves.

Figure 3: Articulating our Investment Philosophy

Source: Taylor Financial Group

3. Who is your custodian?

While a financial advisor may offer guidance and financial advice, the custodian will help clients complete transactions.

Practice tip: Prospects will want to research your custodian since you as the advisor will be working closely with that institution. Have the information they need ready at hand so they can do their research.

Figure 4: Offer Clarity on Your Custodian

Source: Taylor Financial Group

4. Are you a fiduciary, and can I get that in writing? What are your core values and what do you stand for?

A fiduciary is a financial advisor who must act in a client’s best interest at all times. A fiduciary cannot recommend a strategy or investment unless it is the best available option for the client. Non-fiduciary advisors, on the other hand, simply need to meet a lower “suitability” standard. What is equally important here is not just the label, but what it actually means. Reassure your prospects that you will act in their best interests and try to resolve conflicts in a reasonable way. And make sure you demonstrate in other ways what you stand for.

Practice tip: If you are not a fiduciary, consider becoming one, as it is an essential step in building trust from the onset of the advisor-client relationship. And also pull together a list of your core values and what you stand for and be ready to discuss that with a prospect.

Figure 5: Be Clear on Core Values

Source: Taylor Financial Group

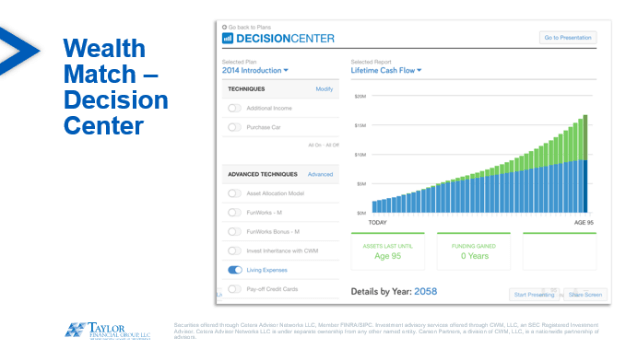

5. Can you stress-test my portfolio to make sure I am taking on the right amount of risk for my situation?

Stress-testing is about assessing the potential impact of economic scenarios on a client’s portfolio and other investments. Discussing how you handle stress-testing with your potential client will show how you identify and adjust potential risks. And of course, explaining your financial planning process will also come in handy here (see the figure below).

Practice tip: Provide examples of actual cases you have presented to clients to show how the stress testing works and how you used the information to benefit clients.

Figure 6: Show Your Financial Planning Process

Source: Taylor Financial Group

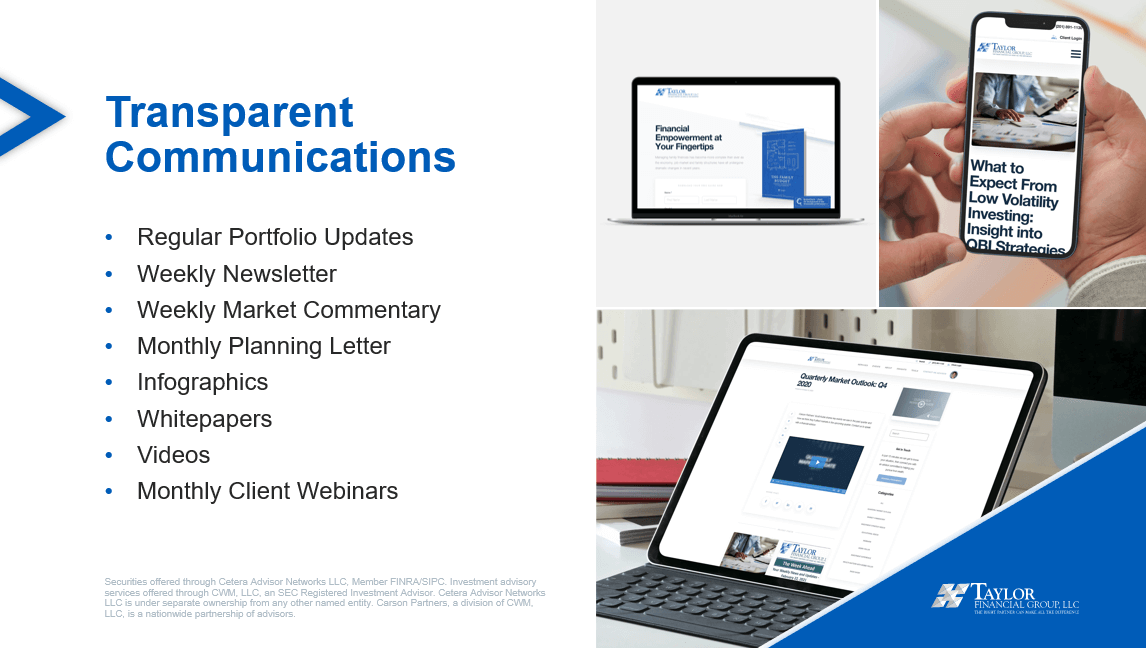

6. How often will you communicate with me to discuss my overall situation?

Another way to view this question is that the prospect is asking “How much access will I have as a client to you, the advisor?” They want to know how often you will meet and whether you are available for phone calls or emails outside of scheduled appointments.

Practice tip: Explain your normal communication schedule and then ask the prospect how often they like to be contacted to customize their experience.

Figure 7: Offer a Regular Communication Schedule

Source: Taylor Financial Group

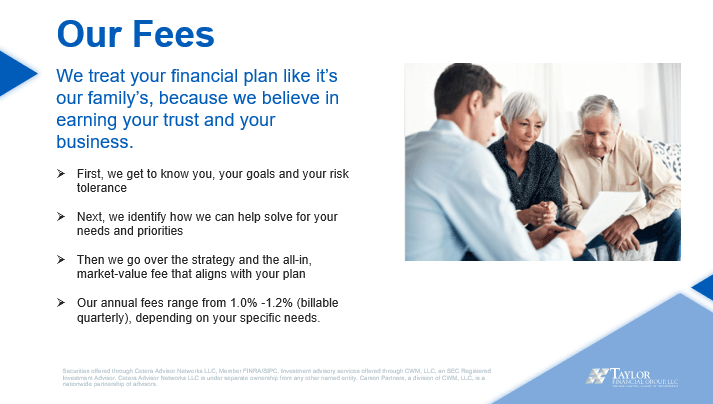

7. How do you get paid? Do you and your firm get paid from any other sources in connection with my business with you?

Advisors can use a variety of fee structures. There are multiple ways advisors get paid, whether it is with a fixed fee, hourly fee, assets under management (AUM), commissions, or some combination of these. Be open and articulate about your fees; illustrate your fees so the prospect knows exactly how it works.

Practice tip: Getting this information to your prospect can help determine if they feel comfortable with how you will be paid, so be transparent. If it’s not a good fit for them or for you, this conversation will help determine that.

Figure 8: Openly Discuss Fees

Source: Taylor Financial Group

8. Will you provide a written, comprehensive financial plan, and how often will you update it?

A financial plan essentially acts as a guide for your client to go through life’s journey. Therefore, financial planning helps clients determine their short and long-term financial goals and creates a balanced plan to meet them.

Practice tip: Providing each client with an updated written financial plan annually, will ensure all aspects of the clients plan are on track with their goals.

Figure 9: Lay Out the Financial Planning Process

Source: Taylor Financial Group

9. Can you assist with reviewing my will, trusts, beneficiaries, or health care power of attorney?

Tied up with these items are the most important financial decisions a client will have to make. Let prospects know you understand that a wrong move with any of these processes could create financial trouble and you are there to look out for their best interests.

Practice tip: Let the prospect know you are happy to work in harmony with their current estate planning attorney—and if they don’t have one in place, you are happy to recommend one. When you are willing to work with a prospect’s other professionals on their behalf, it increases an advisor’s value in the prospect’s eyes. You become part of a team that is looking out for them.

10. Can you help me determine my long-term care funding strategy?

More than half of individuals 65 and older will require some type of formal long-term care services during their lifetimes, and the price tag could leave them in shock. Advisors should be prepared to discuss the different long-term care options available and how they have handled them with different clients.

Practice tip: Give the prospect some real-life examples of how getting your clients long-term-care coverage helped save them money.

11. Can you review my life insurance to make sure I have the right type and amount of insurance?

Life insurance should always be framed inside the overall financial plan. Consequently, a prospective client needs to find an advisor they trust to guide them through decision-making.

Practice tip: The important factor is to never buy without considering the impacts on a client’s overall financial situation. Hence, as their advisor, you need to reassure them all of this will be addressed.

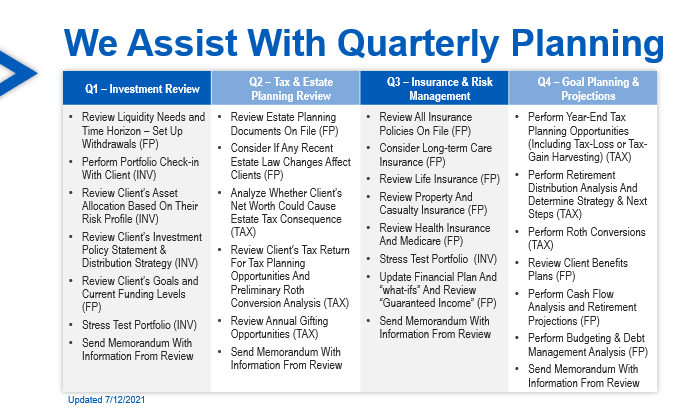

We include our quarterly planning themes, with Q2 dedicated to Tax and Estate Planning Review and Q3 dedicated to Insurance and Risk Management:

Figure 10: Reassure Prospects all Bases Are Covered

Source: Taylor Financial Group

12. How do you consider taxes as part of my overall situation?

Taxes impact nearly every aspect of a client’s life, and being conscious of that issue in a financial plan can save your client thousands of dollars each year. A discussion with your potential client about taxes helps ensure they understand that you have their tax bill in mind when making financial decisions.

Practice tip: Asking about taxes and fees is a gateway for prospective clients to explore their estimated net return, so discuss how working with you can help in this area.

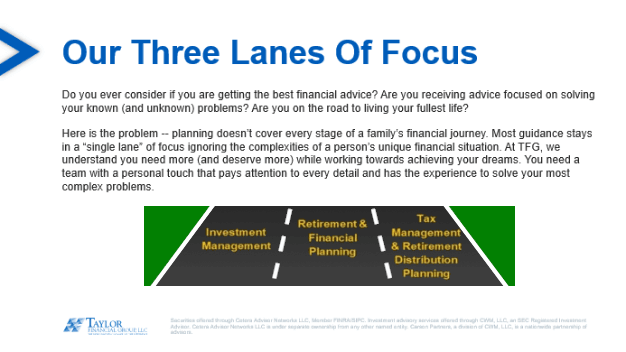

We include the following slide, “Our Three Lanes of Focus” in our discovery presentation. This opens the discussion on how (1) investment management, (2) retirement and financial planning and (3) tax management and retirement distribution planning all need focus throughout a client’s journey, with some areas needing more focus at certain times during a client’s life.

Figure 11: Assure Prospects That You Focus on the Right Issues

at the Right Times

Source: Taylor Financial Group

Preparing answers to these questions before your first meeting with a prospective client is the first step to a successful relationship.