For any client, particularly for those higher net-worth clients, minimizing taxes is a top priority—the more money that stays in your client’s pocket, the better. And although many advisors are not as sensitive to after-tax returns as they should be, you know better. The more after-tax money your client has, the more their account can grow and the more money you can make as their fee-based advisor. To say nothing of your ability to differentiate yourself.

Although most advisors want to help clients minimize taxes, it is often difficult knowing how to proceed. Earlier we have discussed the need to analyze tax returns as a precursor to doing any type of tax planning. And we have also written about the various software programs that can assist in providing tax analysis. And there is no question, this is a lot of work and requires a fair amount of training and infrastructure.

We now address a slightly simpler way to approach tax planning and a good starting point to a potentially very complicated issue: whether to perform a Roth conversion or do tax loss trading. We frame this as an either/or, although, for some clients, it can be a “both.” But, many clients have a limited capacity for the various tax planning strategies, so often, an advisor is doing one or the other.

The biggest challenge is to know what strategy makes the most sense and for whom, as all things are not created equal, and your choice of strategy can depend on a lot of factors. And to complicate matters even further, there are open tax proposals that will affect your approach to this decision, depending on how future capital gains will be taxed and depending on how Biden treats the taxpayer with over $400,000 in income. Either way, we know that taxes are going up, so these decisions are becoming more and more essential to your practice.

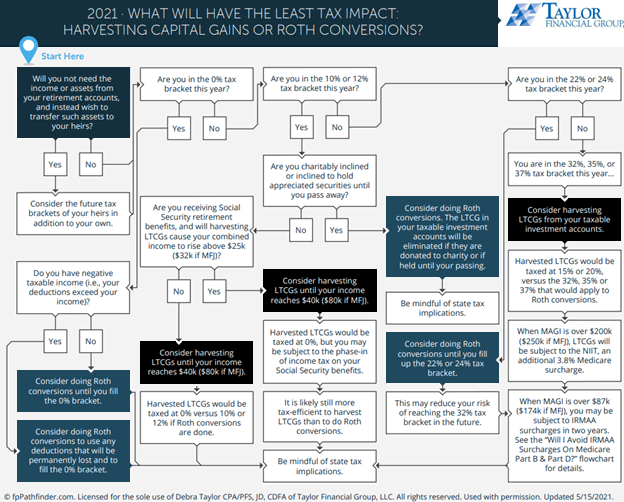

To keep it simple, tax-loss harvesting versus performing a Roth conversion can make more or less sense depending on the client’s tax bracket, so perhaps we should begin the client conversation there. This is where fpPathfinder’s flow chart “Harvesting Capital Gains or Roth Conversions” can provide guidance and simplify the initial process of determining how best to proceed based on your client’s current tax rate. This could be merely the first step, and then you discuss it with the client and step into your tax software for a fuller analysis where you can literally “run the numbers.” Or, for a smaller client, this three-step process can be all you need.

Figure 1: Harvesting Capital Gains or Roth Conversions An fpPathfinder flow chart

Source: fpPathfinder; used with permission.

We summarize below each tax bracket and whether Roth conversions or harvesting capital gains could have a smaller tax impact.

1. Is your client in the 10% or 12% tax bracket this year?

Then harvest long-term capital gains until income reaches $40,000 for single ($80,000 for married filing jointly).

For clients in the 10% or 12% ordinary tax bracket (but still in the 0% capital gains tax bracket), it’s often better to harvest capital gains (versus performing a Roth conversion and thereby generating ordinary income) as the capital gains will not be taxed as long as income stays below $80,000 if married filing jointly (MFJ). By harvesting gains at the 0% rate, a taxpayer can reduce the impact of future capital gains being taxed at the 15% capital gains rate. (And thus minimizing a 15% increase in capital gain taxation from 0%.) Remember that harvesting gains will increase overall income, but you are still ahead as you could see a 15% increase in the capital gains tax bracket, compared to a 10% increase, from 12% to 22%, in ordinary income tax.

Remember that harvesting capital gains in this situation may make some or all of the income subject to the Social Security tax. Having said that, it still may make more sense to harvest the capital gains, despite any additional tax, but numbers can be quickly run for your client’s situation to prove the case.

2. Is your client in the 22% or 24% tax bracket this year?

Then perform Roth conversions until you increase income to $164,925 for single and $329,850 for MFJ to fill the 24% tax bracket.

Once your client is into the 22% and 24% tax brackets, capital gains quickly become subject to an 18.8% tax rate (15% capital gains tax plus Net Investment Income Tax of 3.8%). Being at the 18.8% capital gains rate leaves only a potential 5% increase at the top capital gains rates (23.8%), while ordinary income tax rates jump by 8% to the next (32%) tax bracket (and can climb further from there to 35% and 37%).

Note the increase in ordinary income rates comes sooner (the 32% tax bracket begins at $164,926 for individuals or $329,851 for married couples) than the increase in tax brackets for capital gains (which doesn’t kick in until $445,850 for individuals or $501,600 for married couples). This makes it more appealing to fill up either the 22% or 24% tax bracket with Roth conversions and pay tax at the lower ordinary-income rate.

A word of caution: don’t forget that when MAGI is over $87,000 for single ($174,000 for married filing jointly), you may be subject to IRMAA surcharges in two years. The tax software will illustrate this for you so you can incorporate it into the recommendations.

3. Is your client in the 32%, 35%, or 37% tax bracket this year?

Then consider harvesting long-term capital gains from your taxable investment accounts, as the preferenced long-term capital gains tax rate of 23.8% (don’t forget the NIIT) is still far lower than the 32%–37% tax rates from the ordinary income tax brackets.

For those in the 32%, 35%, or 37% ordinary income tax bracket, harvesting long term capital gains would be taxed at 15% or 20% (plus 3.8% NIIT), versus the 32%, 35%, or 37% that would apply to Roth conversions. In addition, as discussed above, when MAGI is over $200,000 for single ($250,000 for married filing jointly), capital gains will be subject to the NIIT, an additional 3.8% Medicare surcharge. And as income increases, Medicare IRMAA surcharges could grow until MFJ income exceeds $750,000.

If your client is looking to take advantage of tax savings strategies—whether a Roth conversion or capital gain harvesting—start by reviewing their taxable income and tax bracket and then consider the decision tree above as a starting point.

Post script

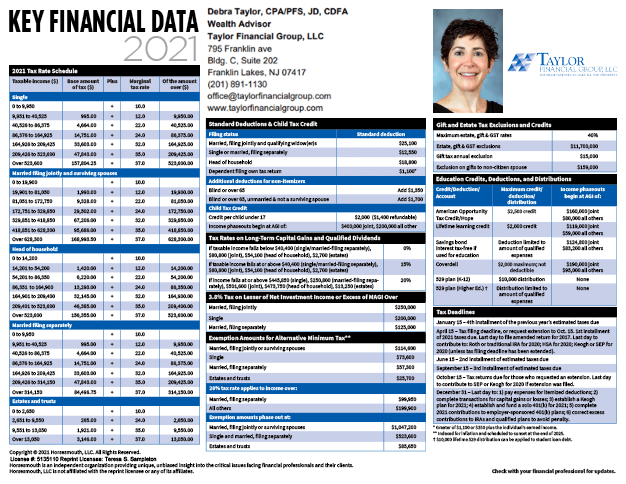

For reference, we have included the Horsesmouth 2021 Key Financial Data resource below so you can see where your client falls on the tax rate schedule. This handout acts as an indispensable resource to me when meeting with clients.

Figure 2: 2021 Key Financial Data Card

Source: fpPathfinder; used with permission.