So you are hunting for the big client—the kind you train for your entire career. But before you get them on board, you’ve got to develop the game plan to handle that UHNW client. That’s because the game is slightly changed for big clients: a $20 or $30 million client will require similar strategies to that of an $8 or $10 million client, but will also require additional strategies simply due to the additional wealth and potentially taxable assets, and you need to be prepared for that.

I experienced these issues first hand when we recently brought aboard a “self-directed” $35 million couple. He was in his late 90’s, had done no estate or tax planning, and held concentrated positions in individual stocks to the point where one stock comprised 40% of the portfolio. And this was just the beginning of the issues we had to address. I discuss below some of the strategies that we put to work immediately.

1. 529 Plans

Gift split, get money out of the estate, and help family all at the same time

Most massively wealthy clients will be at a later stage in life and will likely have either children or grandchildren who will need to pay for college. I recommend that our wealthy clients fund Section 529 plans for their younger relatives. Current law allows gift-splitting and five-year frontloading up to $150,000 per beneficiary without filing a gift tax return. Funding 529 plans helps your client’s family while immediately drawing down the total estate value—and it is all so simple!

For our wealthy client, we funded $1 million towards multiple 529 plans for five beneficiaries. To get the breakpoint, we chose to fund an even $1 million, and thus we funded plans over the $150,000 per beneficiary. However, we were already filing a gift tax return for other giftings we were doing, so it wasn’t an issue to do that here (and it isn’t a big deal anyway). And just a note, you can gift up to $500,000 for some of these 529 plans, so don’t be stingy if you don’t have to be.

Remember, the total gift to the 529 plans will only be removed from the taxable estate if both spouses survive for five years from the date of the account opening (and there will be pro-rating of the gift if one spouse dies before the five years are up). Even so, we would be no worse off if this happened.

And regardless, the beneficiaries still reap the benefits of 529 plans, which allow for tax-free growth and tax-free distributions when used for qualified education expenses. So, the earlier and more generous, the better. Although, as an aside, don’t forget that direct gifts can be made to the institutions without any limitations.

- Essential question: Does the client have young relatives that they want to help?

2. Highly appreciated stock

Contribute to a charitable foundation to save on taxes and assist others

You’re likely familiar with the work of at least a few foundations, including the Bill and Melinda Gates Foundation. Your wealthy client can form their own foundation and reap several benefits while donating to the charities they would like to support. When a private foundation is created, the client can have relatives or advisors serve as foundation trustees, and you can continue to manage the investments held by the foundation.

They can also select the “public charities” they would like to benefit on a year-by-year basis as recipients of funds from the foundation. Note that after their first year of existence, private foundations are required by law to give away an amount that at least equals five (5%) percent of the value of its assets each year.

The foundation allows the client to contribute appreciated securities held in their personal investment accounts. For example, if your clients contribute $1 million to the private foundation, not only do they avoid capital gain recognition on the appreciation of the portfolio when the foundation sells those assets, but they would (1) an income tax deduction for the charitable contribution based on market value, and (2) avoid the 56% combined estate/inheritance tax rate on the $1 million placed with the charity. This would save another $560,000 of potential Federal estate and New Jersey inheritance tax. Note that when a foundation sells appreciated securities, it only pays a minimal excise tax on the gain (1.39%).

However, make note that if the foundation is selling appreciated stock, it cannot be seen as doing anything pre-ordained, as the transaction could then be disallowed. Also remember that all charitable contributions are subject to the AGI limitations of 30%-50%, depending on the type of private foundation. And finally, remember the private foundation is not your client’s personal piggy bank, so formalities must be followed.

- Essential question: Is your client already donating to charity? Do they own appreciated stock? Do they want to assist the next generation in learning about philanthropy?

3.Qualified charitable distributions

Drive down your client’s tax burden

Most of your older clients typically will have large balances in a traditional IRA account. One way to drive down a client’s tax burden is to have your client make a qualified charitable distribution (QCD).

Donating funds to a charity directly from an IRA allows the transfer to be treated as a non-taxable event, thus helping clients avoid a potentially high ordinary-income tax rate, which currently stands at 37%. A QCD also counts as a required minimum distribution (RMD) from an IRA in the year the transfer happens.

To qualify for this special tax treatment, your client must be at least 70½ years old at the time of the transfer. There are limits to this strategy: the maximum annual QCD allowed is $100,000 per taxpayer. A married couple, thus, can double this amount to $200,000 if both make a QCD. One client saved 50% by foregoing the RMD in favor of the QCD once state and other taxes were factored in.

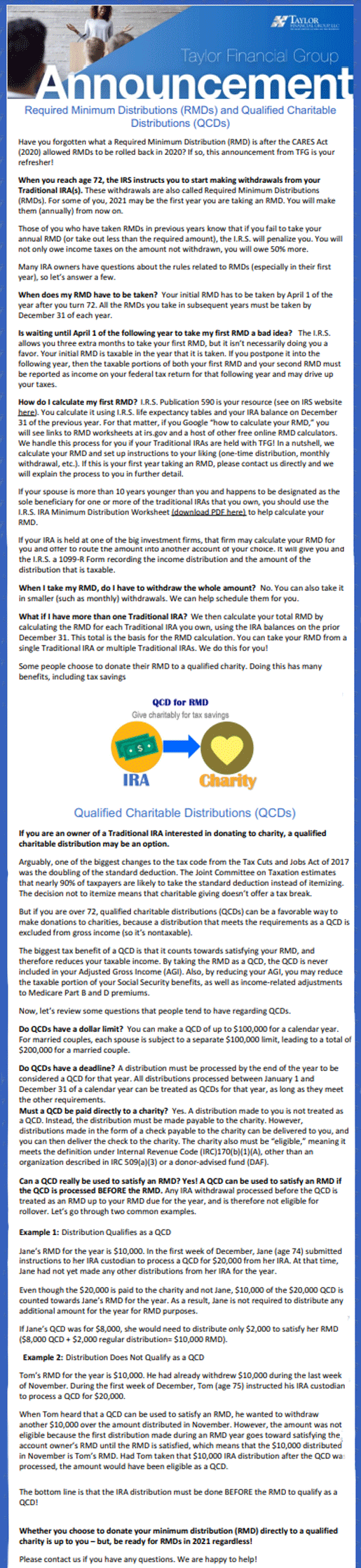

Also, certain charities—including donor-advised funds, private foundations, and supporting organizations—aren’t eligible to receive QCDs. And remember that the QCD will also assist the clients two years later when calculating IRMAA surcharges. Figure 1 below shows a sample of the announcement Taylor Financial Group sends to clients regarding QCDs.

- Essential question: Is your client over 70½ years old, and do they have a large traditional IRA balance? Are they interested in driving down taxes and benefiting charity?

Figure 1: Alerting Clients to the QCD Opportunity

Source: Taylor Financial Group

4. Family Limited Partnership (FLP) or Family LLC

Decrease the value of the estate and contributing to the continuity of the family wealth management

The FLP is a solution for the client whose children have graduated college, have already funded their 529 plans to satisfaction, or have so much money that more extraordinary measures must be taken. The technique is to create a holding company structure (a partnership-like vehicle called a “limited liability company” or “LLC”) to hold securities.

Instead of holding the securities individually, an LLC owned by the client becomes the property owner of the securities. Because of restrictions that will appear in the Company’s operating agreement that limit a partner’s ability to cash out, the tax law typically recognizes discounts in the 15%-25% range, helping drive down the value of your taxable estate.

For example, creating a holding company with $10 million of marketable securities and getting the benefit of a potential 25% discount would allow over $2.5 million of asset value to “disappear” for estate and inheritance tax calculation purposes. Remember to follow the corporate formalities and not get greedy when funding the LLC or applying discounts.

There is no minimum period needed to hold an FLP/LLC for it to be effective. However, if one owner gifts assets to the second owner to use for a contribution to the FLP/LLC, the original owner can only receive the assets back with a step-up in basis if it was held by the second owner one year or more. If held for less than one year, the assets would be returned to the original owner with their own initial basis of the assets.

- Essential question: Are you qualified to set up an FLP and willing to follow the corporate formalities? Do you have family assets that would make sense to contribute to this entity?

Estate planning is essential for all clients regardless of net worth. However, the stakes are typically higher, and the estate planning techniques become more complex with ultra-high-net-worth clients (around $20 million or higher). Whether you already landed the self-managed $35 million client or have one on deck, the four estate planning strategies above can help prove your value and help to reduce estate taxes for your client’s benefit and their family’s benefit in the future.