Inflation has hit everyone hard this past year, and although it is starting to soften, those living on fixed sums are nervous about their reduced spending power. Though the Fed has adopted hawkish policy to stem this inflation, raising its benchmark rate several times in 2022, consumers remain wary of higher costs and the Fed’s ability to contain high costs. The University of Michigan’s Index of Consumer Sentiment measured 59.1 in December of 2022, down 16.3% year-over-year, showing more Americans were searching for reasons to be jolly this past holiday season.

But is there any silver lining to offset the pain of inflation for consumers? The University of Michigan further reported that “about 60% of consumers have already scaled back their spending in response to inflation, and even more consumers plan spending cuts in the year ahead.” In addition, “consumers report more awareness of news on inflation than in the 1970s, which may influence their attitudes.” Surprisingly, financial advisors say yes—2022’s persistent inflation wasn’t all bad news, and there are multiple inflation-adjusted benefits that clients can take advantage of, particularly those who are above the age of 65.

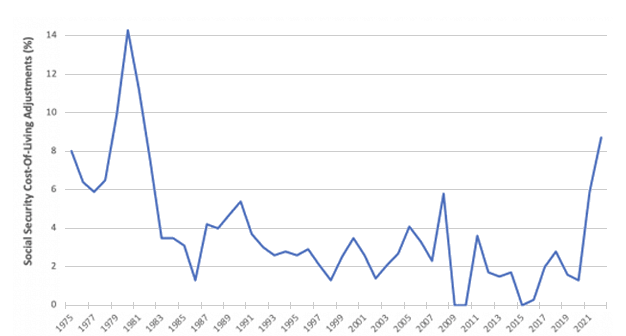

1. Social Security COLA boost

Beneficiaries rejoice at increased checks in 2023 after 8.7% cost-of-living adjustment in 2022.

The 1935 Social Security Act established much of Social Security as we know it today—but, for decades, any increases were a matter of legislation and Congress. That all changed in 1972, when President Richard Nixon signed legislation automatically incorporating an annual cost-of-living adjustment (COLA) to Social Security benefits. The COLA was designed to automatically offset the decrease in purchasing power brought by inflation, with the automatic COLA coming into effect in 1975.

Inflation in 2022 peaked in June at 9.1%, according to the Bureau of Labor Statistics, marking the largest increase in 40 years. With such high inflation, the 2022 COLA adjustment is also elevated at 8.7%, up from 5.9% in 2021 and 1.3% in 2020, providing a cushion for those collecting. This is the highest COLA since 1981, when CPI averaged 8.9% and the COLA adjustment was 11.2%.

Figure 1: Social Security Cost-of-Living Adjustments 1975–2022

Source: Social Security Administration

Note:The 1975–82 COLAs were effective with Social Security benefits payable for June in each of those years; thereafter COLAs have been effective with benefits payable for December. Prior to 1975, Social Security benefit increases were set by legislation.

As a result of the COLA, Social Security and Supplemental Security Income (SSI) benefits for approximately 70 million Americans increased 8.7% in 2023. According to SSA, this 8.7% COLA began with benefits payable to more than 65 million Social Security beneficiaries in January 2023, while increased payments to more than 7 million SSI beneficiaries began on December 30, 2022.

This provides a welcome cushion for older clients who are taking Social Security, especially as this increase won’t be adversely corrected in coming years. This means that, even if inflation falls later this year, the COLA will remain at 8.7%, which could increase the real (inflation-adjusted) value and purchasing power of the Social Security benefits.

This high COLA is accompanied by decreased Medicare Part B premiums. Notably, Medicare Part B covers “physician services, outpatient hospital services, certain home health services, durable medical equipment, and certain other medical and health services not covered by Medicare Part A” according to the Centers for Medicare & Medicaid Services (CMS). According to the Centers for Medicare & Medicaid Services, this decrease in premiums is attributable to “lower-than-projected spending on both Aduhelm and other Part B items and services.”

The savings from this Alzheimer’s drug were able to be transferred to Medicare beneficiaries via a surplus in the Supplementary Medical Insurance (SMI) Trust Fund. This decrease provides further relief for those who are the beneficiaries of Medicare, especially as medical care costs as measured by the BLS have increased 4.2% in the 12 months since November 2021.

Practice pointer: Inform your clients how their Social Security payments might be increasing come 2023 given the 8.7% COLA and varying benefit rollout schedules. Also discuss how they can budget their spending to account for the opposing effects of the COLA increase, Medicare Part B premium decrease and persistent inflation.

2. Brackets ease

Tax bracket bonanza allows clients to stay ‘lower for longer.’

While tax rates will stay the same from 2022–2023 (at 10%, 12%, 22%, 24%, 32%, 35% and 37%), tax brackets (or the levels of income that move clients between tax rates) won’t. Though tax brackets are annually adjusted for inflation, 2022’s pronounced price increases have led to more drastic-than-normal changes. For example, for those filing single, the 10% marginal tax rate kicks in $725 or 7.06% higher in 2023 than 2022, at an income level of $11,000 instead of $10,275; the 37% marginal rate, meanwhile, applies to singles earning over $578,125 in 2023, $38,225 or 7.08% higher than in 2022.

For those married filing jointly, similar increases apply, with 2023’s 10% marginal rate kicking in at $22,000 (up 7.06% from $20,550 in 2022) and the 37% marginal rate coming into effect for amounts over $693,750, up 7.08% or $45,900 from $578,125 in 2022. These expanded brackets provide those with cash flow flexibility an opportunity to reduce their overall tax bill for 2023—one pretax dollar of income received in December of 2022 can have a different after-tax value than in January of 2023.

Standard deduction rises

That’s not all the good news, especially for those over the age of 65. The IRS provides annual tax inflation adjustments for more than 60 tax provisions, including the standard deduction as well as marginal tax brackets. From 2022–2023, the standard deduction for married couples filing jointly will rise by 6.95% to $27,700. The standard deduction for single taxpayers and married individuals filing separately will also rise by 6.95% from 2022 to $13,850, and for heads of households, it will rise by 7.22% to $20,800.

In 2023, taxpayers over the age of 65 or who are legally blind can claim an additional $1,500 in deductions, and $1,850 if they are claiming single or head of household filing status (increased from $1,400 and $1,750 in 2022). And, for those who are both over 65 years of age and blind, the deduction amount is doubled. So, a household married filing jointly where both partners are over 65 could claim a standard deduction of over $30,000 (with the 2023 deduction amount totaling $27,700 + $1,500 + $1,500 = $30,700).

| Expanded Tax Brackets for 2023 |

| Tax rate |

2022 Single |

2023 Single |

2022 MFJ |

2023 MFJ |

| 10% |

Up to $10,275 |

Up to $11,000 |

Up to $20,550 |

Up to $22,000 |

| 12% |

$10,276 to $41,775 |

$11,001 to $44,725 |

$20,551 to $83,550 |

$22,001 to $89,450 |

| 22% |

$41,776 to $89,075 |

$44,726 tp $95,375 |

$83,551 to $178,150 |

$89,451 to $190,750 |

| 24% |

$89,076 to $170,050 |

$95,376 to $182,100 |

$178,151 to $340,100 |

$190,751 to $364,200 |

| 32% |

$170,051 to $215,950 |

$182,101 to $231,250 |

$340,101 to $431,900 |

$364,201 to $462,500 |

| 35% |

$215,951 to $539, 900 |

$231,251 to $578,125 |

$431,901 to $647,850 |

$462,501 to $693,750 |

| 37% |

Over $539, 900 |

Over $578,125 |

Over $647,850 |

Over $693,750 |

Source: Taylor Financial Group, Kiplinger’s, IRS

How does such a high standard deduction affect clients? For starters, any potentially deductible expenses may not create a deduction, and perhaps clients should think of these expenses differently. For example, instead of writing a check to a charity where there will be no deduction, perhaps a QCD makes more sense. Or, this is where bunching of deductions could make more sense and committing to itemizing only every other year.

Practice pointer: As a result of being able to stay “lower for longer” in a tax bracket, some clients may consider timing their income. Clients with flexibility around deductions should decide to itemize only every other year, to take advantage of the widened marginal tax brackets and potentially decrease the effective tax rate they pay in 2023. They may also consider more Roth conversions in 2023.

In closing, the concern with widespread, persistent inflation is that it decreases consumers’ real purchasing power, which is measured by taking the nominal (or “sticker”) rate and subtracting inflation. Higher inflation, then, means lower real purchasing power, and a constant income will purchase consumers a smaller basket of goods and services than it would have previously.

Thankfully, inflation provides two silver linings in 2023 thanks to the SSA and the IRS: an 8.7% COLA for Social Security beneficiaries, to ensure that the value of the benefits isn’t deteriorating in real time, and expanded tax brackets that offer clients an opportunity to reduce their effective tax rate if they play their cards right. Be proactive in reaching out to clients to educate them on what this means for their situations, and the value-add of proper planning.