“ Ethical decisions ensure that everyone’s best interests are protected. When in doubt, don’t.”

—Harvey Mackay, businessman and author

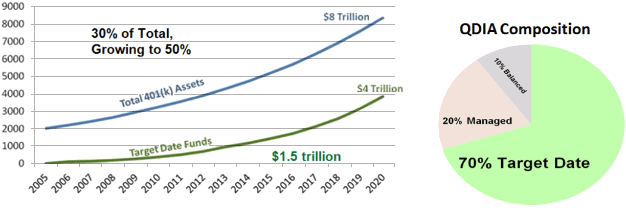

Target-date funds (TDFs) are the most popular investment in 401(k) defined contribution pension plans. They are on a growth trajectory that will take them to $4 trillion by 2020, from their current level of $1.5 trillion. That’s 30% per year growth over the next four years!

On a percentage basis, TDFs will increase from 30% of all 401(k) assets to about half. There are currently 20 million participants in TDFs across 100,000 401(k) plans, and new subscribers default into TDFs every day. Approximately half of all new contributions are going into TDFs, and this percentage will increase to over 60% in just a few years, according to research by Cerulli Associates.

Figure 1: TDFs Will Constitute Half 401(k) Assets by 2020

Source: Ron Surz

The 20 million participants in TDFs tend to be younger since auto-enrollment places new employees in default investments until they make an investment selection. Accordingly, median account balances are small at around $15,000, but the average TDF account balance at retirement is $90,000. In other words the TDF marketplace consists of millions of small accounts that in aggregate total $1.5 trillion. Also, it comes as no surprise that account balances are highest for those nearing retirement, reinforcing the existence of a “risk zone” spanning the 5-10 years before and after retirement that heavily impacts retirement lifestyle due to what is called “sequence of return risk.”&v=y0usszrwsugp3zeg0m5ulz2q

Precarious prudence without legal protection

Despite their growing popularity and importance, there is a lot of confusion surrounding target date funds. Some of this confusion leads to bad decisions that can harm beneficiaries and should expose fiduciaries to legal action, although no one was sued for such investment losses in 2008. When beneficiaries are harmed by well-intentioned but misinformed fiduciaries, restitution is warranted because fiduciaries—plan sponsors and their advisors—should know better. In this case, the defenseless are millions of “little guys” with an average account balance of $90,000 at retirement, paying 100 basis points each to be in TDFs.

The law didn’t protect beneficiaries from TDF investment losses in 2008; not a penny of the 30% or higher loss was recovered. From an ethical perspective, no one likes to see the little guy get hurt, but the law allows it, or at least it did in 2008. We all want what is fair and just. As a practical matter, the applicable legal requirements for TDFs are fulfilled with “procedural prudence,” namely acting as other experts act in a similar capacity. In fact, as you’ll see in this article, TDF fiduciaries rely on procedural prudence and the safe harbor protection of TDFs as Qualified Default Investment Alternatives (QDIAs). But this is not sound ethical practice since it does not protect beneficiaries.

There is some hope on the horizon in the form of the Best Interest Standard of the DOL Fiduciary Rule, which would benefit TDF participants immensely if it does eventually pass.

The Best Interest Standard is an ethical principle that will have legal teeth if the Fiduciary Rule goes into effect. “Best interest” is akin to the fiduciary “duty of care,” which obligates fiduciaries to do the best they can and to do no harm. It’s like our duty to care for our children. And this is the level at which fiduciaries should be operating whether or not the DOL rule is enforcing the standard. The Hippocratic Oath of TDFs should be “First, lose no beneficiary’s money.”

If the DOL’s Fiduciary Rule goes into effect, fiduciaries may be surprised by an aspect of fiduciary law that holds them to a higher standard called substantive prudence, which is doing what is best. A Best Interest Standard demands substantive prudence.

Best interests of beneficiaries

There are four specific areas where TDF fiduciaries should already be applying that substantive prudence, and serving the best interests of beneficiaries:

- Try to select the best

- Protect, especially near the target date

- Avoid excessive fees

- Be wary of gimmicks

1. Selecting the best

Fiduciaries currently believe they are protected by two safe harbors in their selection of TDFs:

- Properly structured TDFs are Qualified Default Investment Alternatives (QDIAs) under the Pension Protection Act of 2006.

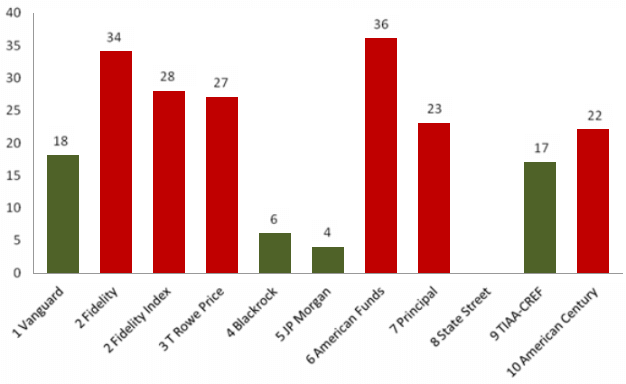

- Choosing one of the most popular TDF providers is procedurally prudent. Fidelity, T. Rowe Price, and Vanguard manage 65% of the blossoming TDF market primarily because they are the largest bundled service providers.

These beliefs fall in the “empty head but good heart” wishful thinking category. They are neither prudent nor ethical because little effort has been made to find the best. Rather, bundled service providers are chosen out of convenience and familiarity. Vanguard, Fidelity, and T. Rowe Price are fine firms, but their target date funds are not the best for everyone, as Figure 2 below shows.

The current data shows that the top 10 TDF managers are not the most prudent. In the following graph we show the Prudence Ranking for the Top 10 TDFs. We’ve ranked the 41 largest mutual fund TDFs. A low rank is good—1 is the best. As you can see, only four of the top 10 are above median in prudence, with a rank below 21. (We don’t have data for State Street.) There are many more prudent TDFs that are not currently popular. Prudence is not currently popular.

Figure 2: Prudence Rankings—Top10 of 41 TDFs

Source: Ron Surz

2. Protect, especially near the target date

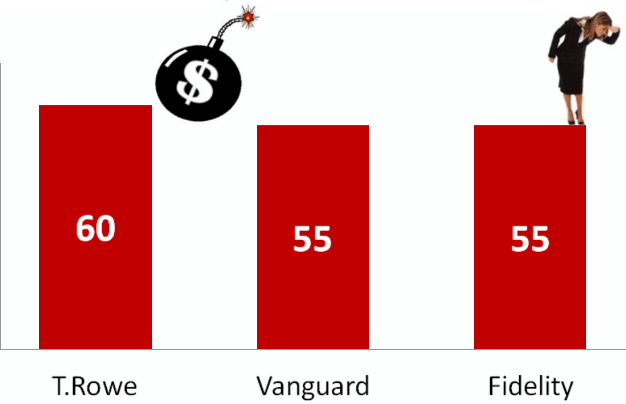

In 2008, 2010 TDFs lost more than 30% and there was a public outcry to never let such losses happen again, especially to those in or near retirement. It was a shocking wake-up call. Beneficiary lifestyles were devastated while at the same time fiduciaries not only went unscathed, they were unphased, choosing to increase risk in the years that followed. Rather than correcting 2008’s problem, TDFs have become riskier because (1) U.S. equity allocations have increased in order to compete in the performance horserace and (2) bonds have become very risky because of quantitative easing.

Equity allocations of the Big 3 at the target date remain at least as high as they were in 2008, as shown in Table 3, and most other TDFs have similar ending allocations. Sixty-five percent of total TDF assets are with these three bundled service providers. There is little or no vetting. Can fiduciaries honestly say they embrace this much risk at target date?

Figure 3: Risk at Target DateEquity allocations of the Big 3 are still way too high

Source: Ron Surz

Just because fiduciaries got away with large losses in 2008 doesn’t mean excessive risk is right or that fiduciaries will continue to get away with it. The basic ethical dilemma here is that TDFs are being sold, not bought, and what is being sold is not safe. You can’t blame the fund companies because they are not fiduciaries; they’re vendors whose business is selling profitable products.

Since most participants either withdraw their assets or purchase an annuity when they retire, the duration of TDF assets should more closely approximate the participant’s retirement date. In other words, allocations at the target date should be very safe, mostly in short term bonds. Prior to the Pension Protection Act’s declaration of QDIAs, the common practice was to default participants into cash or stable value. This may have been too conservative for younger employees, but it was just about right for those nearing retirement.

3. Avoid excessive fees

Books were written and T.V. shows were aired about the excessive fees in 401(k) plans, but nothing changed until lawsuits were won. As reported by the 401(k) HelpCenter&v=y0usszrwsugp3zeg0m5ulz2q, the list of litigants is long and includes Insperity, Allergen, TIAA, J.P. Morgan, Wells Fargo, Oracle, T. Rowe Price, Aon Hewitt, Edward Jones….

When it comes to fees, a best interest standard already exists thanks to lawsuits. Fiduciary interests are aligned with beneficiary best interests. So now fund companies are racing to the bottom on fees because fiduciaries fear lawsuits. Lawsuits are the stick that changed this unethical behavior. It’s a shame that ethical behavior requires successful lawsuits, but that has been the history of such matters.

4. Beware of gimmicks

Not surprisingly, opportunists have entered the TDF game, including custom funds, market timing, and ESG funds.

Encouraged by the DOL’s 2013 Tips, some vendors are selling custom target date funds as a means to match workforce demographics. These one-size-fits-all glide paths cannot match a diverse group of employees. The best “custom” fund matches the one demographic that all defaulted participants have in common, namely a lack of financial sophistication. In other words, safety first is the way to match the one demographic that can actually be matched.

Another gimmick is market timing, modifying the glide path in response to a vendor’s crystal ball predictions. The implied promise is that these providers will get out of the way of the next 2008. Time will tell of course, but history suggests that this is a very tough call. A more reliable course of action is to use a glide path that always protects near the target date.

The most recent gimmick is ESG (Environmental, Social, Governance) Funds, intended to make the investor feel good. Since TDFs are chosen by fiduciaries rather than participants, the good feeling is targeted to fiduciaries. Under a best interest standard, fiduciaries would be required to focus on more important matters, like selecting the best and controlling risk at the target date.

Bottom line

Target date funds should be bought, not sold. With $1.5 trillion in TDFs, the stakes are much higher today than they were in 2008 when TDFs were $150 billion—only 10% of current assets.

Incentives modify behavior and come as carrots and sticks. Ethical decisions that protect employees are the carrots. Fiduciaries can feel proud for doing the right thing. Yet ethics did not motivate fiduciaries to seek low fees. Sticks, namely successful lawsuits, got the job done.

And so it may take the passage of the DOL Fiduciary Rule and its enforceable Best Interests Contract to get fiduciaries working to the standard which they should already be meeting today. It is unconscionable for fiduciaries to jeopardize a dignified retirement for even a single participant. Ethical fiduciaries will research and implement superior alternatives for defaulted participants. It’s equally unconscionable for asset management companies to market TDFs under the wrong premise—that being performance over prudence. TDF beneficiaries need and deserve the best interest standard and fiduciaries should be providing that right now, whether the law comes into play eventually or not.