More and more, taxes are in the headlines. Whether it is SECURE Act 2.0 or the sunsetting of the TCJA in 2025, there is a lot for clients to be worried about. And a lot for you to do.

With all this work, advisors may question whether it makes sense to add tax planning as an additional service to their firm. We discuss below four reasons why tax planning is, indeed, a must-do service for all advisory firms intent on growing and serving high-net-worth clients.

1. Tax planning attracts prospects

Prospects need a catalyst, a reason to change. If they are “doing it themselves,” then they are not paying any fees or they are paying minimal fees. So the idea of paying an advisor an annual fee to provide the same services that they are providing for themselves will obviously not be an attractive proposition to them. However, providing a service—such as tax planning—that they cannot replicate themselves will often create enough value to change their minds.

Investment management and even broad financial planning are often not enough to attract those price-sensitive prospects, as they don’t see enough value in those services to justify an annual fee of just 1%. But in its updated Advisor Alpha Study, Vanguard shows that an advisor who provides services in seven different modules, including services related to tax planning, can typically provide 3% or more in additional net returns.

If your prospect is with another advisor, your offering of tax services will most certainly distinguish you and probably give you one of the best chances of closing this prospect. And the data supports this idea, with over 38% of clients surveyed saying they are willing to change advisors to obtain tax services.

Either way, you need to get prospect’s attention. You need to discuss ideas and concepts that they are not aware of and that can help them. You must go beyond investment management and financial planning. This is where tax planning comes in, now more than ever. Discussing the expiration of the TCJA, the possibility of taxes going up, the SECURE Act, and even the widow’s penalty will get their attention and position you as the specialist.

And to be clear, at Taylor Financial Group, offering tax services has provided enough of a distinction that we have been able to raise our minimums and protect our fee (at about 1%). Indeed, we are often able to close business and attract accounts from other managers, although we are slightly more expensive than others. That is because prospects see the value in what we do and the benefit to themselves.

2. Tax planning helps retain clients

When you provide thoughtful tax planning services, you are not only able to attract new clients to your firm, but you are better able to retain your existing clients. Those existing clients will appreciate the fact that you continue to evolve to serve their needs and welcome the opportunity to work deeper with you. Remember, these clients have already bought into your value proposition and they already believe in you. The fact that you are stepping up even more for them will engender faith and further cement the relationship, as they know they are working with a true professional.

Our experiences over the last few years have demonstrated time and time again that clients will leave their advisor for another advisor who can better serve them in tax planning, even if that new advisor is more expensive. A recent Charles Schwab Study shows that 81% of RIA firms are providing tax planning and strategy, while 68% are providing estate planning.

So remember, if you don’t offer those services, someone else will. Don’t leave yourself reacting to these situations or losing your valuable clients because you didn’t take advantage of this opportunity.

3. Providing tax planning helps grow AUM

Advisors may not think of this aspect, but providing tax services enables you to grow your AUM. How is that? Beyond the obvious that you are attracting prospects and retaining existing clients (see above), you are also positioning client portfolios for larger values by employing tax optimization in your investment and planning work.

How so? Doing Roth conversions allows you to drive down RMDs later in life and ultimately drive down the lifetime tax bill, which enables accounts to grow more. And distribution planning enables your clients to withdraw money from their accounts in the most tax-effective way, ultimately allowing these accounts to grow.

Imagine that you engage in tax planning of all types for all of your larger clients. Think about how much value you bring to the relationship and how much value you literally bring to the accounts, sometimes hundreds of thousands, even millions, of dollars over each client’s lifetime. And in turn, each of these accounts will add up to a higher AUM for your firm.

4. Taxes are on your client’s mind and you need to help

Your clients care about taxes, regardless of their party affiliation or how patriotic they are. And this is where things may have changed, even from just five years ago, when taxes may have been just an afterthought. A recent Financial Advisor Magazine study shows that 69.7% of firms provide tax planning, and 51% of clients use those services when offered.

Clients are currently sitting on large account balances courtesy of the 11-year bull market that has only recently ended. Markets are uncertain. Clients are living longer. Interest rates and prices are higher. And tax laws are changing, often not in your clients’ favor. This is all adding up to the proverbial perfect storm—our wealth needs to work harder, last longer and therefore needs to be taxed less.

Taxes are ultimately the common enemy and the fight against higher taxes allows you to sit on the same side of the table with your client. I had a conversation the other day with a $9 million prospect couple who had their assets with three different custodians and had previously paid little to no fees.

They were facing imminent retirement, and they had amassed over $5 million in their retirement accounts without realizing the adverse taxation that they would be facing. In addition, they were still working well into their 70s, owned income-producing real estate, and also had over $6 million in taxable accounts. They had assumed that they would have lower taxes in retirement, so their small fortune in tax-deferred accounts would not be a problem. You can imagine that they were fee-sensitive, and the idea of paying us $70,000 in annual fees was a shock to them.

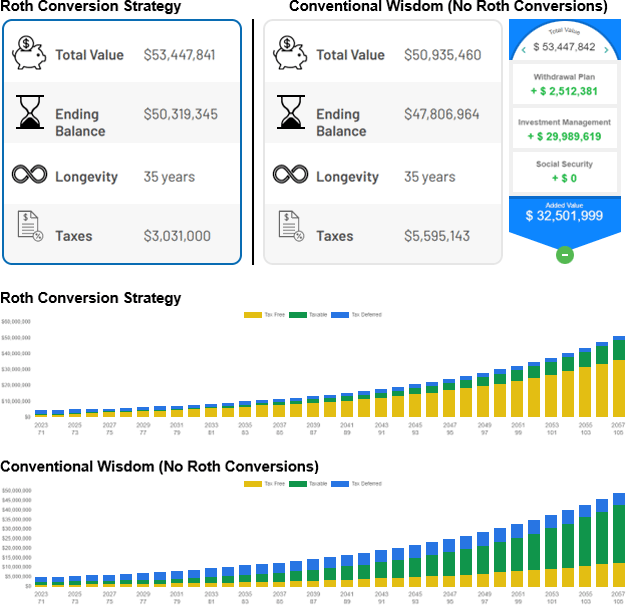

I patiently showed them a case study of lifetime tax savings and wealth creation for a couple with $2.5 million in retirement assets (see the figure below) so they could see the tangible financial benefits of working with us. This case study couple had a younger spouse who had a pension (so the assets would accumulate for a longer period of time) and there was less lifetime drawdown due to her Social Security and her pension.

A Case Study in Tax-Planning Results

Source: Taylor Financial Group

We reviewed the case study together and I pointed out the savings at the bottom of the page, which included a $2.6 million tax savings for the couple in the case study. I quite simply said to them: You can choose whom to pay—a little to me in the form of your annual fee, or a lot to the government down the road in the form of higher taxes. Most will choose the former. They did.

Also what is very compelling here is the additional $24 million in tax-free assets remaining after the second spouse passes! Lastly, I reminded them that the case study only addressed one aspect of our services, and that there were many other ways we intended to bring value to the relationship. They were sold.