Editor’s note: For 2018, our Top 10 most popular articles of the year show that advisors were especially interested in the impact of the new tax law, the changing landscape for advisor fees, and new technology. Rounding out the crop were perennial topics touching on professionalism, client service, and effective marketing. From more than 500 articles published this year, Horsesmouth members rated this as one of the best.

The Merriam-Webster Dictionary defines the word “evergreen” as “retaining freshness or interest” or something that is “universally or continually relevant.” As financial advisors in this new age, our services should reflect these same characteristics. Not only because we need to show clients the value in what we offer, but because providing superb service is the only way to justify our fees. In a nutshell, we need to give clients what they need (and want) before they even know they need or want it. We need to stay on the cutting edge. And we have some ideas on how to do it.

Why AUM fees are becoming difficult to justify

To start, we need to remember why fees based on AUM are a real problem for financial advisors, especially those who do no more than manage investments. First of all, let’s get one thing clear—most financial advisors, including us, built their practice on AUM. There’s no shame in that, because it used to work well. In fact, it was considered the honorable way to charge clients (instead of the commission-based model) because it showed that the financial advisor’s interests were aligned with the client’s. It is transparent and we only got paid based on how the client’s investments performed. Totally fair! Right?

Unfortunately, this is no longer the case. First, it’s now becoming apparent that clients expect much more than just investment management. Oftentimes, they even want less investment management or none at all, and more financial planning instead. Second, for the past several years, we have been dealing with the increasing threat of the robo-advisor. The way the client sees it, especially if they’re only interested in investment management, they shouldn’t have to pay any more than what a robo-advisor charges. The rebuttal argument is clear for us—a robo-advisor simply can’t give clients the service or experience that we can. That’s easy for us to understand, but we need to deliver on this promise and it’s not always so easy for the client to recognize.

Right now, the average advisor is charging their clients somewhere between 100–110 basis points. In other words, the average AUM fee is around 1% for an account worth about $1 million. The problem with that is that big, dominant companies like Vanguard and Fidelity Investments are charging half of that and sometimes even less. Clients have trouble seeing past the numbers. All they see is that we’re charging double the price. So how can we compete? How do we justify our fees?

Year-round services that go above and beyond

Last year, we started working on building out year-round services in a more structured way, so that we are constantly working on finding solutions for our clients, without ever waiting for clients to ask us and without tying services to appointments. The truth is that most clients don’t even know what we’re supposed to do for them. So, we shouldn’t be waiting for them to ask us to do what we already know we should be doing. We found that for clients that aren’t consistently engaged with us throughout the year, the most effective way to do this was by creating quarterly planning checklists that would help us address our four main planning areas. The key point is to “wow” clients by being proactive and consistent.

Q1: Investment review

In the first quarter of the year, we focus on the investment review. We like doing this in Q1 because it’s the start of a New Year and it’s a good time to make sure your clients’ investments are on track, as well as confirm that they are still aligned with their risk tolerance. Naturally, we prioritize by segmentation, starting with our A+/A clients first, and working our way down. First, we review all of the client’s accounts to make sure that everything is accurate and up to date, including accounts that are not managed by us. Then, we review when the client last took our risk tolerance questionnaire, to see if it’s necessary for them to take another one (if it’s older than a year), and to confirm that we’ve taken their risk tolerance into consideration in their portfolio.

As we review the client’s portfolio, we pay close attention to specific details. Is their asset allocation still on track? Is anything underperforming? What’s the benchmark comparison? Should the portfolio be adjusted pursuant to recent market trends? We also take this time to review the client’s 401(k) plans, their contributions to other investment accounts, and their liquidity options as compared to potential cash flow needs.

Once we’ve checked all the boxes (literally), we then send an email to the client highlighting our review and analysis, and we provide any recommendations we may have.

Q2: Estate planning

Because estate tax laws can be complex and so many things can change in a year (personally and legally), we believe having a complete estate planning review once a year can be extremely helpful to the client. Most clients have been told (by attorneys or other professionals) that they don’t need to review their estate plan any more than every three to five years, or if there is a significant change in circumstances. That may have been true in the past, but with the new tax law changes, it is no longer true. We think an annual review is a safer bet, and we’ve seen time and time again how an annual estate plan review reveals important facts.

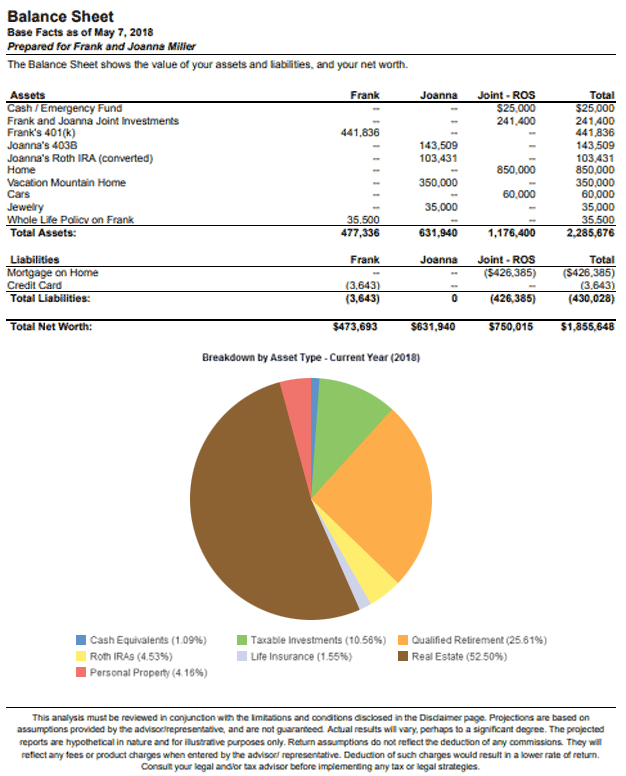

During the Q2 review, we consider how the current estate tax laws may affect the client. We also update (or create) a list of assets for the client using eMoney, including personal property and life insurance, which then generates a balance sheet, giving the client a full financial picture.

Sample eMoney Balance Sheetfor fictional clients Frank and Joanna Miller

Source: Debbie Taylor

We also review beneficiaries, executors, guardians and trustees for potential updates, compare the client’s estate plan with their account titling, confirm that we have copies of all estate documents on file, and make estimates of estate taxes to evaluate tax consequences and/or savings (and any need for life insurance).

Once we’ve gone through all of the items on the Q2 Planning Checklist, we send the client a summary of our findings, request any necessary documents, and provide whatever, if any, recommendations we have.

Q3: Risk management

This is another area of service that we believe is essential to the client’s financial plan and deserves its own annual review. This type of review is effective because there is so much involved with managing risk and making sure your clients are adequately covered by insurance. It’s also effective because you can oftentimes find that clients have insurance policies that they shouldn’t even have, and you can save them money while converting that money into investable assets.

Our risk management review includes checking emergency funds, as well as reviewing life insurance policies, long-term care insurance, disability insurance, property and casualty insurance, and health insurance. We then provide the client with a complete overview and analysis of their insurance coverage and information, and we let them know if we have any recommendations.

Q4: Cash flow management, tax planning and retirement planning

The end of the year brings about an in-depth look at the client’s cash flow, tax planning and retirement planning. This is when we take the time to review debts and liabilities, and we figure out if the client’s discretionary funds are being properly invested or used to pay down debt. We even create a cash flow analysis and budget that we review with the client.

We also request that clients provide us with copies of their tax returns (if they didn’t do so earlier in the year), and we dig deep into their returns to determine if there are any ways we can save them money on taxes before the end of the year. We go further by reviewing the client’s taxable income to see if we can make any adjustments to get them to a lower bracket. We also review how the client’s Social Security is being taxed (if applicable), determine if there is potential for tax loss harvesting on accounts, and review the client’s remaining annual gift exemption, among other things.

Retirement planning is the last part of our Q4 review. Here, we perform a complete and thorough review of the client’s WealthMatch™ (our branded version of eMoney), including their portfolio, to make sure the client is still on track toward pursuing their goals. We also determine how engaged the client has been with their WealthMatch™ plan and personal dashboard, and we consider what we can do to get them more engaged.

Like with the other quarterly reviews, once we’ve completed our assessment, we send the client a full summary and analysis, address any issues or concerns, and provide recommendations.

Keeping clients aware

Having these quarterly reviews is not only effective in terms of helping keep clients on track, but it also helps clients see how much we do for them. It shows them that we are always working for them, not just once a year when we meet with them to review their portfolio, but all year round. And, most important, it maintains consistent communication throughout the year, which opens the door to conversations with clients that would otherwise not be possible.

With this high level of service, things hardly ever fall between the cracks, and clients feel like they’re getting the best bang for their buck!